Crafting a Sustainability Plan: An Essential Guide

- Hussain Parpia

- Jul 23, 2024

- 4 min read

Updated: Nov 8, 2024

Creating a corporate sustainability plan involves setting clear, actionable goals based on the strategy pillars decided in the overall corporate sustainability strategy. This plan outlines specific initiatives and projects that drive sustainability performance, ensuring the organization not only complies with regulatory demands but also actively contributes to a sustainable future. Here’s a essential guide to developing a sustainability plan, integrating key financial analysis tools and frameworks to ensure effective implementation and measurable outcomes.

1. Establishing SMART Objectives

Setting SMART (Specific, Measurable, Achievable, Relevant, Time-bound) objectives is crucial for a successful sustainability plan. These objectives provide clear targets and timelines for the organization’s sustainability efforts, ensuring accountability and facilitating progress tracking. Importantly, SMART objectives should align with the strategy pillars decided in the overall sustainability strategy to ensure coherence and focus.

Specific: Clearly define what the organization aims to achieve. For instance, "Reduce greenhouse gas emissions by 25% by 2025" is more precise than "Reduce emissions."

Measurable: Establish metrics to track progress. This could include carbon footprint, energy consumption, water usage, waste generation, or social impact indicators.

Achievable: Set realistic goals that the organization has the resources and capability to achieve. This might involve incremental improvements or pilot projects before scaling up.

Relevant: Align objectives with the organization’s core values, business strategy, and the strategic pillars defined in the sustainability strategy. Ensure that sustainability goals support overall business objectives and stakeholder expectations.

Time-bound: Specify deadlines for achieving the objectives. This helps maintain focus and urgency and allows for regular progress reviews.

2. Financial Analysis and Justification of Initiatives

Figure 1: MACC, Source - CEEW

Figure 2: SROI, Source - Lind Foundation

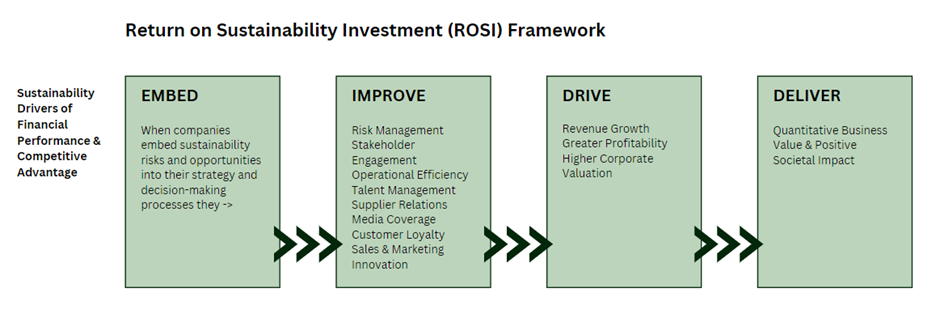

Figure 3: ROSI, Source - NYU Stern

Integrating financial analysis into the sustainability plan is essential to demonstrate the value and viability of sustainability initiatives. This involves using various financial tools to evaluate the cost-benefit of projects and ensure they contribute to the organization’s financial performance.

Cost-Benefit Analysis: Assess the financial costs and benefits of each initiative. This includes direct costs (e.g., equipment, materials) and indirect costs (e.g., training, maintenance), as well as the financial benefits and negative externality mitigation (e.g., cost savings, revenue generation, GHG emissions).

Margin Abatement Cost Curve (MACC): Use the MACC to identify and prioritize cost-effective ways to reduce negative externalities such as GHG emissions. This tool helps in understanding the financial implications of different emission reduction initiatives and selecting the most cost-effective options.

Return on Sustainable Investment (ROSI): Evaluate the broader financial impact of sustainability initiatives using ROSI. This approach considers both tangible and intangible benefits, such as improved brand reputation, increased customer loyalty, and enhanced employee engagement.

Social Return on Investment (SROI): Calculate the social value created by sustainability initiatives using SROI. This involves quantifying social and environmental benefits in monetary terms, providing a comprehensive view of the value generated by sustainability efforts.

3. Implementing Initiatives and Projects

With SMART objectives in place, the next step is to develop and implement specific initiatives and projects that will drive sustainability performance. Each initiative should be carefully planned, resourced, and monitored.

Project Planning: Develop detailed project plans for each initiative, outlining the scope, resources needed, timelines, and key milestones. Assign project managers and teams to oversee implementation.

Resource Allocation: Ensure that sufficient resources—financial, human, and technical—are allocated to each initiative. This may involve investing in new technologies, training employees, or hiring additional staff with specific expertise.

Monitoring and Evaluation: Establish a system for ongoing monitoring and evaluation of initiatives. This includes setting up data collection mechanisms, conducting regular progress reviews, and adjusting plans as needed based on performance data.

4. Embedding Sustainability in Operations

To ensure lasting impact, sustainability must be embedded into the organization’s core operations and culture. This involves integrating sustainability principles into daily business activities and decision-making processes.

Policy Development: Develop and implement policies that support sustainability objectives. This could include procurement policies favouring sustainable suppliers, energy management policies, or waste reduction policies.

Employee Engagement and Training: Engage employees at all levels in the sustainability journey. Provide training and resources to help them understand their role in achieving sustainability goals and encourage their participation in sustainability initiatives.

Sustainable Supply Chain Management: Work with suppliers and partners to ensure they adhere to sustainability standards. This includes setting sustainability criteria for supplier selection, conducting regular audits, and collaborating on sustainability projects.

5. Measurement

Effective measurement is critical for tracking progress and demonstrating accountability. Regular measurement also facilitates continuous improvement by providing data that can inform strategic adjustments.

Performance Metrics: Use key performance indicators (KPIs) to measure the impact of sustainability initiatives. Financial metrics should include cost savings, revenue growth, and improved risk management, while non-financial metrics might cover social and environmental impacts.

Continuous Improvement: Regularly review and update the sustainability plan based on performance data and changing external conditions. This ensures the plan remains relevant and effective over time.

Conclusion

Developing a corporate sustainability plan is a multifaceted process that requires setting “SMART” objectives aligned with strategic pillars and conducting robust financial analysis. By integrating tools like MACC, ROSI, and SROI, organizations can ensure that their sustainability initiatives deliver tangible benefits. The journey towards sustainability is ongoing, but with clear objectives and well-aligned initiatives, companies can achieve lasting positive impacts for both business and society.

Comments